Video Transcript:

Many communities in northern Iowa were hit hard by the derecho storm of August 2020.

VanDerGinst Law seeks to help those business owners that have been affected by this terrible natural disaster by helping file claims against their business insurance policy.

You may not even be aware you have coverage available in your policy to get compensation for lost income due to damage and power outages associated with the derecho storm.

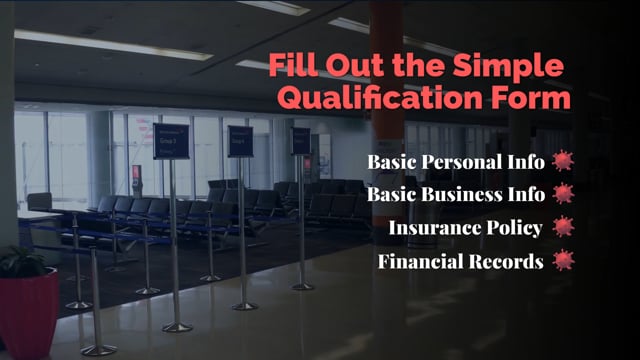

To see if you qualify, visit vlaw.com/derecho and fill out the qualification form.

Provide us with basic information about you and your business, as well as your insurance policy and financial records.

Our team will determine if you have a viable case and the amount you may be eligible for.

It’s a quick, simple process that only takes minutes to complete and the evaluation is free.

Get started today.